Top 6 Apps Like Klarna for Buy now, Pay Later Options

In recent years, the rise of “Buy Now, Pay Later” (BNPL) services has revolutionized how consumers approach online shopping. By allowing shoppers to spread the cost of their purchases over a series of instalments, these platforms have made it easier than ever to manage budgets while enjoying the things we love. Klarna, one of the pioneers in this space, has gained widespread popularity for its user-friendly interface and flexible payment options. However, with the market for BNPL services expanding, several alternatives have emerged, offering their unique features and benefits. Here, we explore the top 6 apps like Klarna that provide similar BNPL options for savvy shoppers.

About Klarna

Klarna, a Swedish financial services company, lets people buy things online and pay for them later (BNPL). It has more than 500,000 business partners in 45 countries and 150 million customers around the world. Klarna offers a number of ways to pay:

Pay in four equal payments over six weeks. Pay 25% of the total price when you buy the item, and the rest in three equal payments every two weeks. There is no interest on this, but there is a $7 late fee if you’re late.

You can pay in 30 days without interest: You can try things on before you buy them with this choice. Since it’s not broken or old, you can return it if it doesn’t fit.

You can pay for something over 6, 12, or 24 months. If you choose this method of payment, the interest rate is 17.9%, and there is a $7 late fee if you are late.

Best Companies and Sites Like Klarna

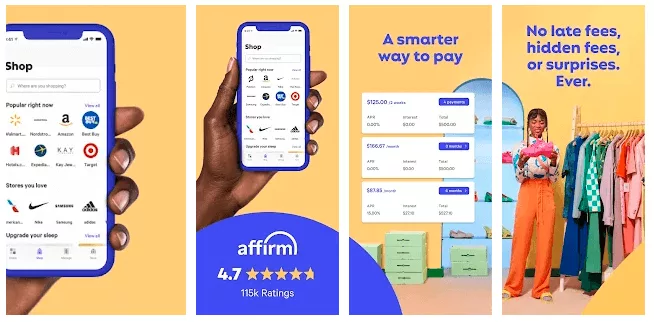

1) Affirm

Apps Like Affirm stands out as a leading app in the point-of-sale lending industry, having been founded in 2012 in San Francisco. With over 40 million customers and collaboration with more than 245k merchants, Affirm offers a seamless shopping experience.

Unlike traditional credit, Affirm allows customers to see the total cost upfront, eliminating surprises. Shoppers can choose between 4 interest-free payments every 2 weeks or monthly instalments with terms that can vary by merchant, including 3-, 6-, and 12-month options at 0-36% interest, making it an incredibly flexible option for those looking to manage their spending without incurring hidden fees.

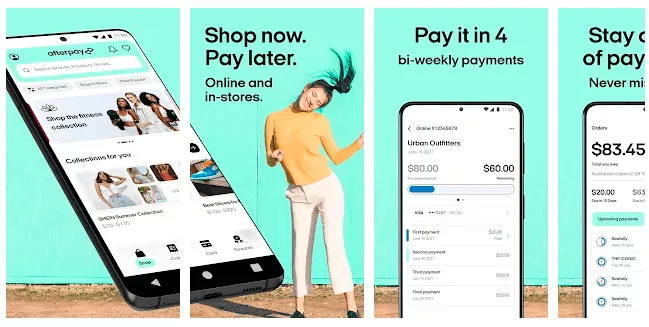

2. Afterpay

Apps like Afterpay is another major player in the BNPL market, offering a straightforward four-payment plan that divides the purchase amount into four equal installments due every two weeks.

One of Afterpay’s distinguishing features is its strict no-interest policy, ensuring customers only pay the price of their purchase. The app also encourages responsible spending by setting sensible spending limits and suspending accounts that fail to make payments on time, thereby promoting financial discipline among its users.

3. PayPal Credit

While PayPal is widely known for its secure payment processing, PayPal Credit introduces a BNPL option that integrates seamlessly with the millions of stores that accept PayPal.

Offering 6 months of special financing on purchases of $99 or more, PayPal Credit provides a flexible and convenient way for shoppers to spread out their payments without interest, provided the balance is paid in full within the promotional period. Its widespread acceptance and the familiarity of the PayPal platform make it a go-to choice for many online shoppers.

4. Sezzle

Apps like Sezzle focuses on empowering shoppers to take control of their financial futures by offering interest-free payment plans. The platform divides the total purchase amount into four interest-free payments over six weeks, with no impact on the customer’s credit score if they pay on time.

Sezzle stands out for its commitment to financial empowerment, providing users with financial literacy resources. This approach not only makes shopping more accessible but also educates consumers about responsible spending.

5. Splitit

Splitit takes a unique approach to BNPL services by allowing customers to use their existing credit card to split their purchase into monthly payments, without the need for additional approvals.

This means shoppers can earn points and rewards on their credit cards while still enjoying the flexibility of instalment payments. With no interest, late fees, or application processes, Splitit offers a hassle-free way to leverage existing credit lines, making it an attractive option for those wanting to maximize the benefits of their credit cards.

6. Zip (formerly Quadpay)

Apps like Zip, known previously as Quadpay, allows users to split their purchases into four equal installments, payable every two weeks. What sets Zip apart is its flexibility; customers can use Zip at any online store that accepts Visa, offering unparalleled freedom in shopping choices.

Additionally, Zip provides a virtual card that can be used for in-store purchases, expanding the possibilities for BNPL beyond online shopping. With a simple and transparent fee structure, Zip is committed to providing a user-friendly experience without hidden costs.

7. CareCredit

CareCredit is a well-known buy now, pay later (BNPL) financing option, commonly used for medical and healthcare expenses. With a CareCredit card, customers can divide their payments into short-term plans lasting around 4 to 6 weeks, similar to installment payment apps like Klarna.

For larger expenses, users can select extended financing plans ranging from 6, 12, 18, or 24 months, up to a maximum of 60 months. CareCredit provides short-term no-interest options, deferred interest plans, and promotional monthly payment plans that may run from six weeks to 12 months or longer.

The card can be used for various services, including medical treatments, dental care, cosmetic procedures, vision care, and select wellness services. The standard maximum financing limit generally goes up to $20,000.

Wrap Up

As BNPL services continue to grow in popularity, these platforms offer a range of options catering to different needs and preferences. Whether you’re looking for a service with a vast network of merchants, one that rewards financial responsibility, or a platform that integrates with your existing financial tools, there’s likely a BNPL service that fits the bill.

By providing flexible payment options without the burden of traditional credit, these apps are redefining how we approach our shopping experience, making it more accessible and manageable for consumers everywhere.

FAQs

What’s Better: Klarna or Afterpay?

Klarna and Afterpay both provide Buy Now, Pay Later (BNPL) services, including pay-in-4 installments and monthly payment plans. However, there are some differences in flexibility and market presence. Klarna offers additional options such as a “Pay in 30 Days” feature, giving users more payment choices. Afterpay is widely used for smaller retail purchases and is especially popular among younger shoppers who prefer straightforward, short-term installment plans. Klarna, on the other hand, is often chosen for higher-value purchases. Ultimately, the better option depends on your spending habits and payment preferences.

Klarna vs. Sezzle: Which One Is Better?

Klarna operates in over 45 countries and supports larger transaction amounts along with flexible repayment terms. Sezzle primarily serves users in the United States and Canada. It provides accessibility through a virtual card that can be used both online and in physical stores, and it is known for accommodating users with limited credit history. Businesses seeking a simple and fast setup may lean toward Sezzle, while those targeting international markets and broader customer bases may find Klarna more suitable.

What Are Some Other Apps Like Klarna and Afterpay?

Several other BNPL platforms offer similar installment payment services. These include Affirm, Sezzle, Zip, FinanceMutual, CareCredit, Sunbit, Denefits, Cherry Financing, PayPal Pay Monthly, ViaBill, Uplift, Amazon Pay Later, PerPay, and PayZen. Each platform varies in terms of repayment terms, approval processes, and merchant partnerships.

What to Consider When Choosing Apps Like Klarna and Afterpay?

When selecting a BNPL provider, it is important to evaluate both financial and operational factors. Key considerations include merchant fees, flexibility in payment plan structures, credit check requirements, repayment terms, approval rates, integration process, and overall user experience. Assessing these aspects carefully helps ensure the chosen platform aligns with business goals and customer expectations.