10 Best Buy Now, Pay Later Apps (Trending)

Buy Now, Pay Later (BNPL) apps have transformed the way consumers approach online shopping, offering a flexible alternative to traditional credit. As we move into 2024, the popularity of these services continues to surge, with more shoppers opting for payment plans that allow them to purchase products immediately and pay over time. This trend is supported by data indicating a significant increase in BNPL transactions over the past few years.

Buy now, pay later (BNPL) is one of the world’s most rapidly increasing financial solutions. In 2021, around 56% of users used BNPL services. So it’s no surprise that consumers like the concept of more flexible payment alternatives at the point of sale, and merchants are seeking for the best methods to enter the market and meet their customers’ demands.

There are numerous BNPL providers, each with a unique approach. As a result, businesses must grasp the distinctions and determine which partner is ideal for them.

Let’s delve into the world of BNPL apps to understand how they work and why they’re becoming a go-to choice for consumers worldwide.

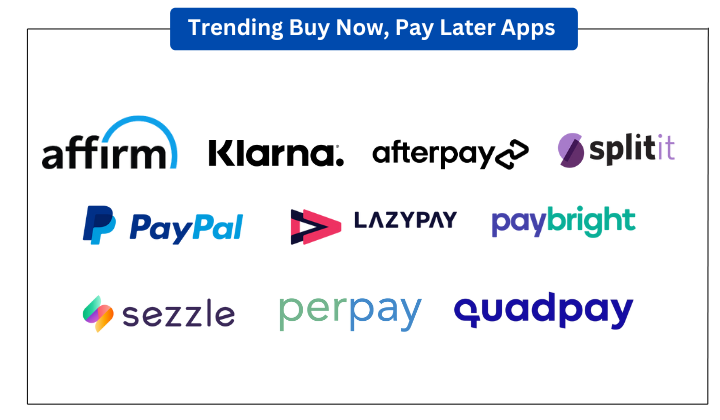

List of Trending Buy Now, Pay Later Apps by AppsInsight

| App Name | Key Features | Requirements | Fees | Supported Locations | Rating |

|---|---|---|---|---|---|

| Affirm | Flexible payment schedules, no late fees, mobile app | 18+, valid U.S./CA address, SSN | Interest varies, no late fees | U.S., Canada | 4.5/5 |

| Klarna | Pay in 4, instant decisions, flexible payment options | 18+, bank account, good credit history | No fee for on-time payments, late fees | Multiple countries including U.S., U.K. | 4.7/5 |

| Afterpay | Split into 4 installments, no credit check for most transactions | 18+, valid email and mobile number, bank account | No interest, late fees apply | USA, Canada, UK, Australia, New Zealand | 4.6/5 |

| Splitit | Use existing credit card, no new debt, flexible terms | Credit card with sufficient limit | No interest, no late fees | Global, wherever credit cards are accepted | 4.4/5 |

| Sezzle | Interest-free installments, soft credit check, reschedule payments | 18+, bank account, email, phone number | No interest, fee for rescheduling | U.S., Canada | 4.7/5 |

| PayPal Pay | Uses PayPal, automatic deductions, no application | PayPal account, legal age, country where available | No interest, late fees may apply | Multiple including U.S., U.K., Australia | 4.5/5 |

| Perpay | Deductions from payroll, builds credit, automated deductions | Employed, steady income, direct deposit capable bank account | No interest or late fees | United States | 4.6/5 |

| LazyPay | Instant credit, minimal documentation, flexible repayments | 18+, valid ID, bank account | No interest if paid within grace period, late fees | Predominantly India | 4.3/5 |

| QuadPay | Part of Zip, split into 4 payments, no hard credit checks | 18+, mobile number, credit/debit card | No interest, fees for late payment | U.S., other Zip regions | 4.4/5 |

| PayBright | Bi-weekly/monthly payments, transparent fees, mobile app | 18+, credit/debit card, resides in supported country | No interest on short-term, late fees for long-term | Multiple countries including U.S., U.K. | 4.2/5 |

About Buy Now, Pay Later Apps

Buy Now, Pay Later (BNPL) apps offer a modern solution for consumers looking to manage their finances more flexibly. These services allow shoppers to make purchases immediately and defer payments through structured installments, often without the need for traditional credit checks that can affect one’s credit score. The appeal of BNPL apps lies in their straightforward, transparent approach to financing—consumers can see the exact amount and number of payments required before committing to a purchase.

This financial model benefits both consumers and retailers. For consumers, it means more control over cash flow and the ability to manage unexpected expenses more smoothly. For retailers, offering BNPL options can lead to higher conversion rates, increased basket sizes, and improved customer loyalty, as shoppers are more likely to complete a purchase if offered a payment plan that fits their budget.

As BNPL services continue to evolve, they are increasingly integrated with major payment platforms and are becoming available across a wide range of e-commerce sites, enhancing accessibility for all types of consumers.

New! Top Sites Like Fingerhut in 2024: Buy Now Pay Later

What’s The Need To Look Fetch Buy Now, Pay Later Apps?

The growing interest in Buy Now, Pay Later apps is not just a trend; it’s a response to the evolving needs of modern consumers. In today’s fast-paced world, where financial flexibility can be as important as the price of a product, BNPL apps provide a necessary bridge. They offer an alternative to traditional credit that is often more aligned with the financial realities of younger consumers, particularly those who prefer not to use credit cards or who may not have extensive credit history.

BNPL apps allow for more strategic financial planning with less risk. The ability to split payments into smaller, manageable parts without incurring interest (if payments are made on time) helps consumers stay within their budget without compromising on their purchasing power. This is particularly important in managing high-cost items or handling emergency expenses that would otherwise require high-interest credit options.

Additionally, these apps come with the advantage of instant approval and minimal paperwork, making them more accessible and convenient than conventional loan products. This ease of use encourages consumers to make purchases they might otherwise delay, boosting consumer spending and supporting economic activity.

Why Do People Use Buy Now, Pay Later Apps?

The appeal of Buy Now, Pay Later (BNPL) apps extends beyond mere convenience. These apps resonate with users for several compelling reasons, which reflect broader shifts in consumer behavior and financial management preferences.

Ease of Use and Immediate Access

BNPL apps streamline the purchase process. Users can apply for and receive approval within minutes, directly at the checkout. This immediacy removes the traditional barriers associated with credit applications, such as lengthy approvals or strict eligibility criteria.

Budget Management

These apps empower consumers to manage their budgets more effectively. By breaking down a purchase into smaller installments, users can align their spending with their cash flow, avoiding the lump-sum expenditures that can disrupt a budget. This is particularly beneficial during high spending periods, like holidays or back-to-school seasons.

No Interest Options

Many BNPL services offer zero-interest plans if the balance is paid within a specific timeframe. This feature is incredibly attractive compared to high-interest credit cards, making BNPL a cost-effective option for many users, especially those who plan their finances to avoid extra charges.

Credit Building Opportunities

Some BNPL providers report payments to credit bureaus, helping users build or improve their credit scores, provided they make payments on time. This aspect of BNPL services is a significant draw for younger consumers who are looking to establish credit histories without the risk of high-interest debt.

Enhanced Shopping Experience

BNPL apps often integrate seamlessly with online retailers, providing a frictionless shopping experience. This integration encourages consumers to make purchases they might otherwise postpone, knowing they can manage the payment terms flexibly.

These factors make BNPL apps not just a financial tool but a lifestyle choice for many, particularly among millennials and Gen Z consumers, who value simplicity and transparency in their financial dealings.

How Do Buy Now, Pay Later Apps Work?

Understanding the mechanics behind Buy Now, Pay Later (BNPL) apps is crucial for both consumers and retailers interested in utilizing this flexible payment option. The process is straightforward, designed to ensure ease of use and accessibility at every step.

Selection at Checkout

When shopping online, customers choose the BNPL option at the checkout. This choice is usually presented alongside other payment methods, such as credit cards or PayPal. Selecting BNPL will lead the customer to a short application process.

Quick Approval Process

The approval process for BNPL services is typically quick and user-friendly. Applicants may need to provide basic personal information, but unlike traditional credit applications, BNPL providers often do not require a detailed credit check. This speeds up the approval and makes BNPL accessible to a broader range of consumers, including those with limited or no credit history.

Immediate Purchase Completion

Once approved, the transaction is completed as usual, and the consumer can take their purchase home or have it shipped immediately. The cost is split into a series of payments that are laid out clearly before the consumer commits to the purchase.

Scheduled Payments

The consumer will pay back the amount over time, according to the schedule agreed upon at the time of purchase. These payments are often automated and deducted from a linked bank account or credit card. Most BNPL plans are structured to be interest-free if the consumer pays on time, though fees may apply for late payments.

Flexibility and Control

BNPL apps provide consumers with flexibility and control over their finances by allowing them to spread the cost of a purchase over several weeks or months. This can make larger purchases more manageable and help users stay within their monthly budgets without accruing significant debt.

The simplicity of the BNPL process and its integration into the everyday shopping experience are key reasons for its growing popularity among consumers of all ages.

Top 10 Best Buy Now, Pay Later Apps in Detail

In this section, we’ll provide a detailed look at each of the 10 best Buy Now, Pay Later apps of 2024. We will cover their unique features, requirements, fees, and more to help you understand how each can fit into your financial planning or shopping habits.

1. Affirm

Affirm offers a transparent and flexible approach to financing, with no late fees or hidden costs. It’s designed for those who value straightforward terms and the ability to manage purchases through an intuitive app.

Affirm provides two payment options, similar to the majority of Buy Now, Pay Later apps: monthly or in four installments. Affirm does not impose late penalties on either of its payment plans, in contrast to other BNPLs. Its Monthly plan does, however, have interest, with the highest rate on our list being 36%. Interest can vary from 0% to 36%.

A mild credit check, order quantity, shopping location, and the selected repayment terms—three, six, or twelve months—will all affect each customer’s APR. Affirm reports some loans, including those with past-due payments, to Experian, which could lower your credit score, even though a soft check won’t have an impact on your credit score.

In addition, Affirm sells three other items. First up is a high yield savings account that has no fees and no minimums. The second option is a virtual card that users may apply for directly through the app and use to make purchases both online and offline. Each card can only be used once.

Finally, consumers who want to make regular transactions can apply for an Affirm Card. Customers can use it as a debit card to make major purchases or pay for products in full after linking it to their bank account. With regard to the latter, customers are able to ask for a payment plan either prior to making a purchase or up to 24 hours afterward.

Requirement

- Must be 18 years or older

- Valid U.S. or Canadian address

- Social Security Number (U.S. only)

Fee/Paid

- No fees for early payments

- Interest rates vary based on creditworthiness and purchase details

Key Features

- Choose payment schedules that suit your budget

- Real-time decision at checkout

- No late fees

- Use Affirm for purchases at thousands of retailers

- Mobile app for easy account management

Supported Locations

- United States, Canada

Rating

- 4.5/5 based on customer reviews

Pros and Cons

- Pros: No hidden fees, flexible payment options, widespread retailer acceptance.

- Pros: No hidden fees, flexible payment options, widespread retailer acceptance.

- Cons: Interest rates can be high for less creditworthy individuals.

2. Klarna

Klarna is known for its “Pay in 4” plan, which splits purchases into four equal payments charged every two weeks without interest.

Klarna sets itself apart from other BNPLs by providing a variety of repayment options. It offers the widely available Pay in 4 short-term loan with 0% interest, along with monthly payment plans that vary from six to 24 months.

There are also other payment options at your disposal, such as Pay Now (yes, you read that correctly) and Pay in 30. Customers have the option to conveniently link their debit or credit cards to pay for items through the Klarna app. If you find the Klarna app useful, this might be of interest to you. Otherwise, it’s just an added bonus.

Pay in 30 is truly exceptional, as no other company on our list provides this option. This option allows customers to place online orders with retailers without any interest charges. After the retailers ship out the product, Klarna promptly sends the customer an invoice. Afterwards, customers are given a 30-day window to determine whether they wish to retain or return the item prior to making payment.

Similar to other BNPL apps, Klarna’s pay-in-four option only necessitates a soft credit check for approval. However, it is worth mentioning that Klarna’s website states that the monthly financing option may entail a hard credit check. One impressive aspect of Klarna’s services is the round-the-clock availability of their customer service through phone and live chat, a feature that sets them apart from other BNPL companies.

Requirement

- Must be 18 years or older

- A bank account in a supported country

- A good credit history

Fee/Paid

- No fee for payments on time

- Late fees may apply

Key Features

- Pay in 4 equal installments, interest-free

- Smoooth shopping app experience

- Immediate decision making

- Flexible payment options

- Partnerships with a wide range of retailers

Supported Locations

- Available in multiple countries including the U.S., U.K., Australia, and more

Rating

- 4.7/5 based on extensive user feedback

Pros and Cons

- Pros: No interest on payments, user-friendly app, extensive retailer network.

- Cons: Possible fees for late payments.

3. Afterpay

Afterpay allows customers to buy what they need now and pay later in four equal installments every two weeks. It emphasizes no upfront fees and quick service during the checkout process.

Afterpay provides customers with two options for financing their purchases: Buy now, Pay later. Customers can opt for Pay in 4, which allows them to conveniently make the first payment at checkout and the remaining three payments every two weeks until the full amount is paid. Pay in 4 does not impose any finance fees or interest, although customers may be subject to late fees. These late fees will not exceed $8 per missed payment, but the total amount of late fees charged can reach as high as 25% of the order value.

Another option provided by Afterpay is a six- or 12-month loan, which requires monthly payments for purchases exceeding $400. This option does incur interest, and the rate will be determined by a soft credit inquiry (an inquiry that does not affect your credit). When considering return customers, Afterpay takes into account their payment history to determine the applicable interest rates.

It’s important to be aware that Afterpay has the ability to report any missed payments to credit bureaus, potentially impacting your credit score in a negative way.

Afterpay’s virtual cards are a notable feature, allowing users to conveniently make in-store payments using either Apple Wallet or Google Wallet.

Although the majority of App Store reviews are positive, there seems to be a recurring trend among Android users on the Google Play store. They have been encountering various issues with the app ever since the update on July 31st, 2023.

Requirement

- At least 18 years old

- A valid and verifiable email address and mobile number

- A bank account in a supported country

- A legal resident of the country where Afterpay is offered

Fee/Paid

- No interest charges

- Late fees apply for missed payments

Key Features

- Split purchases into 4 equal installments

- Automatic deduction from your bank account

- No credit check required for most transactions

- Wide acceptance online and in-store

- Mobile app for easy management

Supported Locations

- Available in countries like the USA, Canada, UK, Australia, and New Zealand

Rating

- 4.6/5 based on user reviews and satisfaction

Pros and Cons

- Pros: Zero interest, transparent fee structure for late payments, wide retailer acceptance.

- Cons: Fees for late payments can add up if not managed properly.

4. Splitit

Splitit stands out by allowing shoppers to use their existing credit card to split their purchase into interest-free monthly payments, without needing to apply for a new line of credit.

Unlike traditional BNPL apps that require setting up a new account or credit line, Splitit simply places a hold on the available balance of your credit card and reduces it as you make payments. This process offers a seamless integration with your financial habits, enabling you to leverage existing credit without undergoing additional credit checks.

The app’s flexibility extends up to 24 months, depending on the retailer and purchase amount, providing substantial versatility for larger purchases. Splitit is particularly beneficial for consumers who already manage their credit well and prefer not to open new lines of credit, maintaining simplicity and transparency in personal finance management.

Requirement

- Must have an available balance on your credit card to cover the purchase

- Credit card from a participating bank

Fee/Paid

- No interest fees

- No application required

- No late fees

Key Features

- Use your existing credit card

- No credit checks or applications

- Flexible payment terms up to 24 months

- Instant approval process

- Reduces the need to acquire additional debt

Supported Locations

- Available globally, wherever major credit cards are accepted

Rating

- 4.4/5 based on global usage and feedback

Pros and Cons

- Pros: No need for a new credit account, utilizes existing credit, no interest or late fees.

- Cons: Requires a sufficient credit limit on your card, less helpful for building credit.

5. Sezzle

Sezzle empowers consumers to purchase now and pay later with its interest-free installment plans. It focuses on responsible spending by performing soft credit checks that don’t impact your credit score.

Sezzle offers three payment options: Pay in 2, Pay in 4, and Pay Monthly, giving users flexibility in their payment choices. Pay in 2 and Pay in 4 both offer 0% interest, while Pay Monthly’s interest rate can range from 5.99% to 34.99%.

Using Pay in 2, customers can split their payment into two installments. They pay 50% at the time of purchase and the remaining 50% the following week. The pay-in-four option functions similarly to other providers, with a 25% down payment at purchase and the remaining three payments made every other week over a span of six weeks. The Pay Monthly option offers flexible payment terms ranging from three to 48 months. The approval for loan amounts will be determined by Sezzle’s banking partners.

Sezzle’s standout feature is its upgrade, Sezzle Up, which allows customers to report their payment history to Equifax, Experian, and TransUnion. This provider is the sole option in our list that offers an opt-in choice for credit reporting. By consistently making timely payments, you can not only boost your spending limit, but also establish or improve your credit history.

Customers have the option to upgrade their account by ensuring timely payment of their orders, setting up their bank account or debit card as the default for scheduled payments, and confirming their personal information with a valid SSN.

Requirement

- Must be at least 18 years old

- A valid bank account in a supported country

- Email address and mobile phone number

Fee/Paid

- No interest fees

- Small fee for rescheduling payments

Key Features

- Split the purchase amount into four installments over six weeks

- Soft credit check only

- Option to reschedule payments (once per order)

- Transparent terms and conditions

- Partnerships with both large and small retailers

Supported Locations

- United States, Canada

Rating

- 4.7/5 based on customer satisfaction and ease of use

Pros and Cons

- Pros: Interest-free payments, minimal impact on credit score, user-friendly interface.

- Cons: Limited flexibility in payment rescheduling, fees for payment adjustments.

6. PayPal Pay

PayPal Pay in 4 lets users split the cost of their purchases into four interest-free payments, made every two weeks. This service is integrated into the PayPal platform, offering a familiar checkout process for PayPal users.

PayPal’s Pay Later offers a pay-in-four plan with a 0% interest rate, similar to other options available. This option is ideal for customers looking to make small or mid-sized purchases, with a range of $30 to $1,500.

PayPal also provides a monthly installment plan for purchases ranging from $199 to $10,000. The interest rate for this financing option varies from 9.99% to 29.99%. Similar to other BNPLs, PayPal customers are required to undergo a soft credit check in order to determine the interest rate applicable to each purchase. Payment for this plan can be made using debit cards and a confirmed bank account, but credit cards are not accepted.

It’s worth mentioning that PayPal Pay Later is not yet accessible in all 50 states. Pay in 4 is currently unavailable for residents of Missouri, Nevada, and New Mexico. In addition, residents of Arkansas, Colorado, Hawaii, Massachusetts, Nevada, New York, and Texas are currently unable to access Pay Monthly.

Requirement

- Must have a PayPal account

- Based in a country where Pay in 4 is available

- Must be of legal age in your respective country

Fee/Paid

- No interest charges

- Late fees may apply

Key Features

- Seamless integration with existing PayPal accounts

- No separate application necessary

- Automatic deductions from linked bank accounts or cards

- Available for purchases between certain monetary limits

- Instantaneous transaction processing at checkout

Supported Locations

- United States, United Kingdom, Australia, among others

Rating

- 4.5/5 based on trust and reliability of the PayPal brand

Pros and Cons

- Pros: Leveraging existing PayPal infrastructure, no interest fees, high consumer trust.

- Cons: Late fees applicable, eligibility restrictions based on purchase amounts.

7. Perpay

Perpay offers a unique spin on the Buy Now, Pay Later model by focusing on micro-installments directly deducted from your paycheck, promoting responsible spending without impacting credit scores heavily.

Users enjoy the benefit of buying immediately while paying incrementally, directly linked to their payroll cycle. This not only ensures timely payments but also fosters financial discipline without the fear of accumulating debt.

Perpay also stands out by offering a product catalog from which users can shop, enhancing the shopping experience. It’s designed for those who prefer a straightforward, automatic repayment plan that aligns with their earning schedule, thereby avoiding late fees and interest charges typically associated with credit payments.

This service is especially advantageous for steady earners looking to balance their spending without impacting their credit scores.

Requirement

- Employment verification required

- Must have a steady income

- Bank account that accepts direct deposits

Fee/Paid

- No interest fees

- No late fees (payments are deducted directly from your paycheck)

Key Features

- Micro-installments deducted from payroll

- No traditional credit checks

- Large catalog of products directly available through the app

- Builds credit with consistent on-time payments

- Easy budget management with automated deductions

Supported Locations

- United States

Rating

- 4.6/5 based on ease of use and customer support

Pros and Cons

- Pros: No interest or late fees, encourages budget discipline, easy integration with payroll systems.

- Cons: Limited to employed individuals with payroll direct deposit, less flexibility in payment scheduling.

8. LazyPay

LazyPay operates as a part of the PayU finance umbrella and offers instant credit at the point of sale with a focus on quick approval and minimal documentation.

It allows consumers to make purchases immediately and pay later, either in one go or through easy EMIs. This service is particularly appealing due to its quick approval process and minimal documentation requirements.

Consumers benefit from LazyPay’s flexible payment options, which help manage cash flow without the need for conventional credit card usage. The app is widely accepted online and at numerous physical stores, enhancing its usability. Designed to encourage responsible spending, LazyPay also provides reminders and automated repayment solutions to avoid late payments, although fees apply if deadlines are missed.

Its accessibility and convenience make LazyPay a preferred choice for many in its operational regions, predominantly India, offering a seamless blend of credit-like benefits with the immediacy of digital transactions.

Requirement

- Must be 18 years or older

- Valid ID proof

- Bank account in a supported country

Fee/Paid

- No interest if paid within the grace period

- Late payment fees apply

Key Features

- Credit limit offered immediately upon approval

- Pay later with one tap at checkout

- Minimal documentation for approval

- Flexible repayment options including one-time payment or EMIs

- Wide acceptance online and at physical stores

Supported Locations

- Predominantly available in India

Rating

- 4.3/5 based on the convenience and flexibility it offers

Pros and Cons

- Pros: Quick access to credit, minimal entry requirements, flexible repayment terms.

- Cons: Fees for late payments, limited geographical availability.

9. QuadPay

QuadPay, a part of the Zip family, allows consumers to split their purchase into four equal installments, paid over six weeks. The service is designed to offer a seamless, interest-free shopping experience without impacting your credit score.

Customers are provided with a unique benefit that sets this provider apart from others – a three-month interest-free period when shopping at select stores.

Zip lacks the option to disable auto pay and imposes late fees, which can result in additional charges such as bank overdraft fees if a payment fails.

Requirement

- Minimum age of 18 years

- A valid and verifiable mobile number

- A credit or debit card from a supported bank

Fee/Paid

- No interest fees

- A small fee is charged if a payment is late

Key Features

- Split payments into four over six weeks

- Instant approval at checkout

- No hard credit checks

- Mobile app for easy management of payments

- Extensive network of partnering retailers

Supported Locations

- Available primarily in the United States, along with other regions where Zip operates

Rating

- 4.4/5 based on user reviews focusing on flexibility and ease of use

Pros and Cons

- Pros: No interest on installments, no impact on credit score for initial check, widespread retailer acceptance.

- Cons: Fees for late payments, dependency on having an active credit or debit card.

10. PayBright

PayBright, a prominent Canadian Buy Now, Pay Later service, offers instant financing options at the point of sale, allowing customers to make purchases immediately and pay over time in easy installments. It’s designed to integrate seamlessly with online and in-store shopping, providing a quick and easy way for consumers to manage larger purchases.

PayBright simplifies budget management without a significant initial impact on the consumer’s credit score, appealing particularly to those who prefer not to accrue credit card debt. Its straightforward application process and direct integration with numerous Canadian retailers make it an accessible and convenient option for a wide range of consumers. PayBright’s approach enhances the shopping experience, allowing customers to buy what they need when they need it while maintaining financial flexibility.

Requirement

- At least 18 years old

- A valid Canadian residency

- A valid Canadian bank account or an approved credit/debit card

- An email address and mobile phone number for verification

Fee/Paid

- No interest on some plans, interest may apply on longer-term financing

- No fees for on-time payments, but late fees apply for missed payments

Key Features

- Quick online application with instant decision

- Pay in 4 for smaller purchases or customized installment plans for larger amounts

- No impact on credit score for initial approval

- Direct integration with a wide range of Canadian retailers

- Automatic account management through the PayBright mobile app

Supported Locations

- Canada

Rating

- 4.5/5 based on customer reviews, highlighting the convenience and flexibility of the service

Pros and Cons

- Pros: Flexible payment plans suitable for a variety of purchase sizes, easy application process, and no initial impact on credit scores.

- Cons: Interest may apply depending on the plan, and late fees for missed payments.

Final Say

The landscape of Buy Now, Pay Later apps offers diverse options tailored to different spending habits, financial situations, and consumer needs. From Affirm’s transparent no-late-fee policy to Zip’s flexible payment schedules for both small and large purchases, each app brings unique benefits and potential drawbacks to consider.

Related FAQs

What is a Buy Now, Pay Later app?

A BNPL app allows you to purchase items immediately and pay for them in installments over time.

How do Buy Now, Pay Later services make money if they don’t charge interest?

BNPL services typically earn revenue through merchant fees and, in some cases, late payment fees from consumers.

Are there any credit requirements for using BNPL apps?

Most BNPL apps perform soft credit checks but don’t require a high credit score for approval.

Can using a BNPL service affect my credit score?

It can, if the service reports to credit bureaus and if you miss payments.

What happens if I miss a payment with a BNPL service?

Missing a payment may result in late fees and can affect your ability to use the service in the future.

Can I return an item bought using a BNPL app?

Yes, returns are subject to the retailer’s return policy, and refunds will adjust your BNPL balance accordingly.

Is there a limit to how much I can spend with a BNPL service?

Spending limits vary by provider and are based on factors like your payment history and creditworthiness.

Can I pay off my BNPL installments early?

Yes, most BNPL services allow early repayments without extra charges.

Are BNPL services available for all types of purchases?

BNPL can be used for a wide range of items, but availability may depend on the retailer and the type of purchase.

How do I sign up for a BNPL service?

You can sign up during the checkout process at participating retailers or directly through the BNPL app or website.

Related Blogs

- Must see! Best Networking Apps For Entrepreneurs, Professional Connections

- Plan your day with Top Shared Calendar Apps – Best of 2024

- Do you know?The Importance of Mobile Applications in Everyday Life (Statistics)